MDIM Journal of Management Review and Practice

Search

Search

1 Centre for Distance Learning, Gandhi Institute of Technology and Management, Visakhapatnam, Andhra Pradesh, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Some countries are actively considering taxing income from cryptocurrency exchanges. In addition to this, in many national and international policy decisions related to Cryptocurrency, regulators also focus on issues such as customer data, money laundering schemes and supporting terrorism. This article intends to examine the regulatory regime of cryptocurrency regulators—from a country-specific perspective.

Bitcoin, cryptocurrency, crypto income, regulatory mechanism, tax policy

Objectives

Introduction

Some countries are actively considering taxing income from cryptocurrency exchanges. In addition to this, in many national and international policy decisions related to Cryptocurrency, regulators also focus on issues such as customer data, money laundering schemes and regulating terrorism. Digital currency can be purchased with fiat money and sold with conventional funds. It can be used to obtain various goods and services. In 2015, in a report entitled ‘Virtual Currency Initiatives: Further Analysis’, The European Central Bank offered a ‘second’ and substantially updated definition of virtual currency.

Review of Literature

Studies on Cryptocurrency/Digital Finance

The idea of cryptocurrency as an open-source platform, a central issuing authority or the seat of a state is new (King & Nadal, 2012). Every investor should have some questions answered (Rogojanu & Badea, 2014): Is bitcoin the oldest particular private currency? Also, how long will it run alongside traditional currencies? In a context of growing discontent generated by the many imbalances emerging in the economies of different countries, is bitcoin able to benefit from a higher level of confidence than it currently has?

Although cryptocurrencies cannot substitute legal currencies, they could influence the global markets, removing hurdles to regulating national currencies and exchange rates (DeVries, 2016). The technology behind cryptocurrency can improve the operations of banks and provide a platform to commence their operations (Raskin & Yermack, 2016).

Bitcoin has shown the way to success, and as of 13 January 2020, the number of bitcoins has reached 5,025 (Caporale et al., 2018). Digital finance comprises of new financial instruments, financial transactions, software used for finance-related transactions and new modes of interaction with customers provided by financial institutions (Gomber et al., 2017). The financial transactions have progressively embedded with technology with the opening of the payment gateway (Gonzalez, 2004). Changes in the prices of bitcoin and the dynamics of mining properties are examined by Corbet et al. (2019).

Indian digital currency exchange is preparing to initiate bitcoin futures. It may be integrated with cryptocurrencies like Bitcoin Cash, Ripple and Ethereum. In addition to bitcoin, there are nearly 1,000 alternative coins (altcoins) of which ‘ether coin’ is the most accepted. Altcoins were introduced after the success of Bitcoin (Rajesh Kurup, 2017).

The price behaviour of cryptocurrencies reveals that the efficient market hypothesis is rejected. However, over the past few years, significant steps towards the effectiveness of cryptocurrencies have been detected. This can lead to speculators adopting less gainful trade strategies (Kyriazis, 2019).

The persistence of the cryptocurrency market, indicating a correlation between its past and future value, is examined by Chaim and Laurini (2018). This study projected a volatility model with discontinuous jumps in cryptocurrency.

Malady (2016) states that ‘while clients may have digital banking for online financial transactions, in many emerging markets they must become online consumers due to a lack of trust in new channels’.

Michael Sockin and Wei Xiong’s (2020) model states that cryptocurrencies are members of a digital platform designed to help users. Cryptocurrency prices must compensate for membership demand, especially the significant complementarity of membership demand, with token supply from speculators, which could lead to a stock market crash.

Yates (2017) points out that the combined turnover of all cryptocurrencies exceeds $100 billion, which can pose a likely hazard to replacing fiat currency issued by banks.

Marian (2015) explains the regulatory regime that imposes anonymity outlay to limit the potentially illegal use of cryptocurrencies. The regulatory authority should restrict various illegal activities like tax evasion, Ponzi schemes, terrorist financing, and so on.

Nara Kim and Jang Mook Kang (2018) analyse blockchain and digital authentication technologies. A digital authentication system is proposed to address the high cost of the existing digital authentication technology.

Dewey & Holland & Knight LLP (2019) examine how governments regulate cryptocurrencies and blockchain technology. It was observed that the blockchain had shown its impact irrespective of geographic boundaries.

However, despite all the attention, visibility and media interest, many have needed help understanding the underpinnings and implications of the technology for policymakers and other officials. The widespread technology adoption across many industries exacerbates this difficulty.

China

Susan and Howard (2010) note, ‘China’s monetary regulatory framework has undergone unprecedented changes in a few relatively short years, and more changes are coming. Chinese banks are large and efficient. China’s monetary framework is generally isolated and not directly affected by global currency issues, although the global slowdown has weighed on trade.

Cai Esheng noted, ‘Relevant laws and guidelines guide China’s financial supervision authorized by the Securities Law at the end of 1998.’ The banking institutions increased from 3,639 in 2007 to 8,721 in 2010, but the value doubled from 51 MB to 6,000 billion.93.2 trillion yuan. In addition, the number of non-bank monetary institutions increased from 690 in 2007 to 782 in 2010, accounting for about 33.1% of GDP, and total resources are estimated at 1,344,442 billion yuan. This has two consequences. First, the number of banking financial institutions has decreased significantly. Second, the increased emphasis on resources reflects the more excellent added value and effectiveness of foundations in the Chinese financial sector.

Russia

Vladimir I. Soloviev (2018) describes the composition and quality of the Russian fintech environment. The results show that the fintech push has yet to cause extreme changes in the Russian economy. This technology is used for online banking, shift management, crowdfunding, blockchain and related activities.

Ponomareva et al. (2020) state, ‘In Russia today, fintech is applied to improve the monetary aspects.’ The respective authorities are assessing the promotion of innovation in artificial intelligence, blockchain and other technological aspects.

Promoting Russia’s fintech development in 2019 involves many issues, including needing an advanced cryptocurrency mining framework, data security issues and the possibility of illegal off-the-shelf transactions due to blockchain innovations.

India

Income on cryptocurrency is taxable in India. The Indian government introduced the Cryptocurrency and Regulation of Official Digital Currency Bill, 2021. This bill was formed to create digital currency issued by the Reserve Bank of India (RBI). On 1 November 2022, the RBI launched the Central Bank Digital Currency in the wholesale and retail market as a pilot project. It is being issued in the same denominations as the paper currency and coins. It is being distributed through the banks.

Crypto Income: Global Tax Regulations

Each country imposes different taxes on digital assets, including cryptocurrencies. Switching from one cryptocurrency to another may be taxable. Spending cryptocurrency on low-value items also is taxable, as it is treated as a sale of cryptocurrency. In the United States, ‘House Financial Services Committee met with the CEOs of major crypto firms to talk about the future of digital assets.’ In South Korea, the regulators have postponed a 20% crypto tax until 2023, citing errors in tax-related data. In Russia, the activities of cryptocurrency are partially regulated.

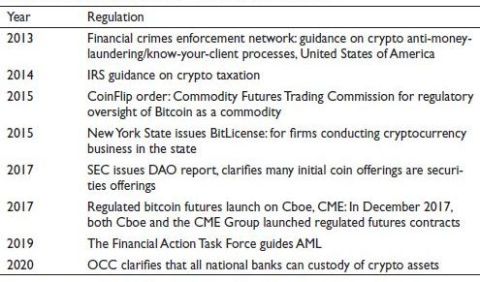

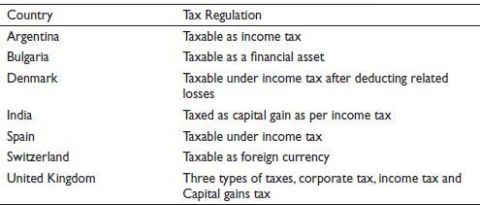

Table 1 depicts the genesis of crypto income regulation during 2010–2020, and Table 2 presents the global tax regulations for cryptocurrency.

Review of Regulatory Mechanisms in Select Countries

China

China is considered the most favoured country for blockchain administration. An administrative order of China, 2013 is ‘Notice to Prepare for the Risks of Bitcoin’. This order granted legal status to cryptocurrency, and it is considered a digital commodity asset.

East Africa

East Africa, as a developing economy, targets digital currencies. Digital currency is similar to mobile protocols useful for lowering transaction costs and accessible to all. Digital payment gateways are helpful to solve challenges further. In particular, virtual currencies may reduce issues relating to the maltreatment of market monopolies caused by fintech companies.

Table 1. Genesis of Crypto Income Regulation: 2012–2020.

Note: IRS, Internal Revenue Service; SEC, Securities and Exchange Commission; DAO, Decentralized Autonomous Organization; CME, Chicago Mercantile Exchange; Cboe, Chicago Board Options Exchange; AML, Anti Money Laundering;. OCC, Office of the Comptroller of the Currency.

Table 2. Global Tax Regulation for Crypto Currency/Digital Asset.

Europe

The European Union released regulations entitled ‘Markets in Crypto Assets’ (MiCa). These regulations are useful to examine the effect of blockchain in financial transactions and assess how to cope with risks relating to crypto-assets. These regulations are encouraging reinforcement of the potential of cryptocurrency. The European Central Bank classified cryptocurrencies as a subset of virtual currencies and it is called unregulated digital money.

South Africa

Darul Uloom Zakariyya of the Islamic Fatwa Centre in South Africa believes that digital currency is allowed by law. The decision meets the property and money criteria and conditions because: (a) it is considered as an asset, (b) it is a medium of exchange, (c) it measures value and (d) it is trading as an account.

India

The RBI has warned investors and traders of digital currencies. Given the cited risks, it has been decided that the entities regulated by RBI shall not deal with or provide services to any business entities dealing with or settling venture capitalists. RBI will study the opportunity of introducing non-mineable bitcoins.

The United Kingdom

The United Kingdom law includes rules laid down in European law. Key considerations are (a) whether the company’s activities related to cryptocurrencies will cause the person to engage in regulated activities that require authorization or registration with the Financial Conduct Authority and possibly the prudent regulator and (b) are there any restrictions on how these cryptocurrencies can be traded and issued in the United Kingdom.

The United States of America

Cryptocurrencies are on the agenda in the United States. The focus is on regulators and agencies within the federal government, including (a) the Securities and Exchange Commission, (b) the Commodities and Futures Trading Commission, (c) the Federal Trade Commission and the Internal Revenue Service and (d) the Department of the Treasury from the Financial Crimes Commission. Despite the significant contributions of these organizations, very little legislation has been enacted. Many state governments have proposed legislation regarding cryptocurrencies and blockchain technology, and it has gone through with most of the work done in the legislature.

The United Arab Emirates (UAE)

The UAE is an advocate of blockchain technology and announced its regulations in April 2018. The UAE Blockchain Strategy 2021 aims to have 50% of all government transactions through blockchain platforms within three years. The program aims to save $11 billion per year, print 398 million documents, travel 1.6 billion kilometres and 77 million man-hours. In Dubai, His Highness Sheikh Hamdan Bin Mohammed Al Maktoum launched the Dubai Blockchain Strategy in October 2016, which aims to make Dubai the first blockchain-powered city by 2020.

Taiwan

Taiwan has not issued any laws or special regulations regarding the rise of certain blockchain technology applications, such as so-called ‘virtual currencies’ or ‘cryptocurrencies’. Taiwan’s financial regulator has issued several publications to educate and inform the Taiwanese people as well as to promote its work on development and behaviour. On 30 December 2013, the People’s Bank of China and the Bank of Taiwan issued a joint press release outlining the government’s stance on bitcoin for the first time.

Venezuela

The Venezuelan government does not approve of cryptocurrencies. He was also responsible for promoting the use of cryptocurrencies and created his own cryptocurrency ‘Petro’. Venezuela has taken additional steps to promote cryptocurrencies, such as special facilities for payments with other cryptocurrencies and special authorizations to ensure that contracts can be paid in their own currency.

Switzerland

The Swiss government’s attitude towards cryptocurrencies and especially the technology behind them is very positive. The Swiss Federal Government and FINMA recognize the potential that blockchain/distributed information technology can provide to the financial services industry and other industries. Switzerland sees an opportunity to become a world leader, and leaders and managers are often open to innovation.

Spain

The Spanish government has been very cautious concerning digital currencies. Spanish law is highly protective of the rights of investors and consumers. Cryptocurrency cannot be legally treated as money for legal tender.

Summary

The following are essential insights observed relating to crypto income regulations across the globe:

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Cai E-sheng. ( 2012). Financial supervision in China: framework, methods and current issues, 169–173. https://www.bis.org/publ/plcy07k.pdf

Caporale, G. M., Gil-Alana, L., & Plastun, A. (2018). Persistence in the cryptocurrency market. Research in International Business and Finance, 46: 141–148. https://doi.org/10.1016/j.ribaf.2018.01.002.

Chaim, P., & Laurini, M. P. (2018). Volatility and return jump in Bitcoin. Economics Letters, 173, 158–163.

Corbet, S., Lucey, B. M, & Yarovaya, L. (2019). The financial market effects of cryptocurrency energy usage. SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3412194.

DeVries, P. D. (2016). An Analysis of Cryptocurrency, Bitcoin, and the Future. International Journal of Business Management and Commerce, 1( 2), 1–9.

Dewey, J. & Holland & Knight LLP (Eds.). (2019). Global legal insights: Blockchain & cryptocurrency regulation 2019 (1st Ed.). Global Legal Group Ltd.

Gomber, P., Koch, J. A., & Siering, M. (2017). Digital finance and FinTech: Current research and future research directions. Journal of Business Economics 87, 537–580. https://doi.org/10.1007/s11573-017-0852-x

Gonzalez, A. G. (2004). PayPal: The legal status of C2C payment systems. Computer Law & Security Review, 20(7), 293–299.

Kim, N., & Kang, J. M. (2018). A case study of public blockchain and cryptocurrency technology focus on authentication system. Journal of Engineering and Applied Sciences, 13(3), 689–690.

King, S., & Nadal, S. (2012). “PPCoin: Peer-to-Peer Crypto-Currency with Proof-of-Stake.” https://decred.org/research/king2012.pdf

Kurup, R. (2017). Future of Cryptocurrencies is here. https://www.linkedin.com/pulse/future-cryptocurrencies-here-rajesh-kurup/

Kyriazis, N. (2019). A Survey on efficiency and profitable trading opportunities in cryptocurrency markets. Journal of Risk and Financial Management, 12(2), 67. 10.3390/jrfm12020067.

Malady, L. (2016). Consumer protection issues for digital financial services in emerging markets. Banking & Finance Law Review, 31(2), 389–401.

Marian, O. (2015). A conceptual framework for the regulation of cryptocurrencies. The University of Chicago Law Review, 82, 53–68.

Ponomareva, M. A., Karpukhin, D. V., & Stolyarova, A. N. (2020). FinTech in Russia under circumstances of I.T. technologies development: Development challenges and solutions. Topical Problems of Agriculture, Civil, and Environmental Engineering, 224,1–6. https://doi.org/10.1051/e3sconf/202022403030

Raskin, M., & Yermack, D. (2016). Digital currencies, decentralized ledgers, and the future of central banking. National Bureau of Economic Research.

Rogojanu, A., & Badea, L. (2014). The issue of competing currencies-case study-bitcoin. Theoretical Applied Economics, 21(1), 103–114.

Sockin, M., & Xiong, W. (2020). A model of cryptocurrencies. Management Science, 69(11), 6687–6707.

Soloviev, V. I. (2018). Fintech Ecosystem and Landscape in Russia. Journal of Reviews on Global Economics, 7, 377–390.

Susan K. B., & Howard, Chao. (2010). The Financial System in China: Risks and Opportunities Following the Global Financial Crisis. Washington, DC: Promontory Financial Group, 7.

Yates, T. (2017). The consequences of allowing a cryptocurrency takeover, or trying to head one off. Financial Times. https://ftalphaville.ft.com/2017/06/07/2189849/guestpost-the-consequences-of-allowing-a-cryptocurrency-takeover-or-trying-to-head-oneoff/